Published on 2 February 2026 (Last updated on 16 February 2026)

In 2026, the office property market in Luxembourg began a gradual recovery after several years of significant economic uncertainty. Following a marked slowdown in 2023 and 2024, the market returned to a more measured and selective dynamic.

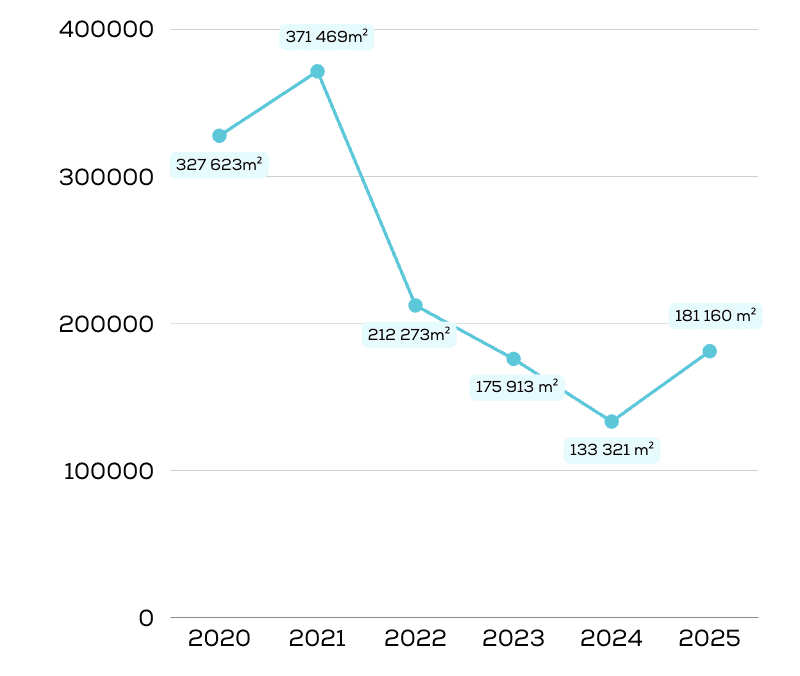

A gradual recovery

The main positive signal from the market is the recovery in office occupancy.

According to recent analyses by JLL, by 2025, leased space will reach 181,160 m², an increase of 36% compared to 2024.

This increase comes after several years of continuous decline since the peak observed in 2021. It does not reflect a return to normal, but rather a gradual recovery, in a context where companies are regaining visibility without abruptly accelerating their real estate commitments.

The transactions mainly concern high-quality properties that are well located and suited to new ways of working. Demand therefore remains targeted, but very real.

Reduction in vacancy rates and alignment of rents

The recovery in the office market is accompanied by a gradual tightening of available supply. The vacancy rate is now estimated at 3.9%, compared with 4.2% in 2023 and 2024, reflecting the market’s ability to absorb new space without any major imbalance. This trend confirms a healthier dynamic, in which supply and demand are gradually returning to equilibrium.

In terms of rentals, the market is showing signs of stabilisation and convergence in values. Rents observed by JLL currently range from approximately €40 to €55 per square metre per month, depending on the sector and the quality of the buildings. This range reflects a market where differences are gradually narrowing, while the best-positioned assets continue to command high levels.

Investment picks up again, but cautiously

On the investor side, the recovery is also visible, but remains moderate.

Investment volumes have not yet returned to their historical levels, but interest in secure assets is gradually returning.

Strategies favour core or core+ properties that are well let, with solid tenants and stable income prospects.

Outlook for 2026: a structured, non-speculative recovery

The outlook for 2026 remains positive but realistic.

The market is expected to continue its recovery at a gradual pace, without a sudden rebound to previous volumes. Demand is likely to remain focused on high-performance, sustainable offices that are suited to hybrid working arrangements.

This development points to a more mature market, where growth is based more on quality, flexibility and sustainability than on expansion of floor space.

Flexiroom: a response to growing mobility

The year 2026 marks an important milestone in the transformation of the office market in Luxembourg. The gradual recovery observed reflects a structural shift in usage patterns, corporate expectations and investment strategies.

This transformation is also redefining residential needs, increasing demand for housing suited to a mobile, international working population. In line with this trend, players such as Flexiroom are naturally fitting into a more agile real estate model, at the crossroads between office and housing.